The Silicon Valley Bank Collapse May Signal The Start Of A New Debt Crisis

The first indication that a financial crisis was brewing, more than 15 years ago, was not the collapse of Lehman Brothers but the one in June 2007 of two hedge funds sponsored by now-defunct Bear Stearns, an investment bank founded in 1923. Their troubles went unnoticed for quite a while, and it wasn’t until more than a year after their downfall, in September 2008, that Lehman Brothers imploded. Things deteriorated very quickly after that.

The collapse of $208B Silicon Valley Bank (SVB) lays bare fragilities in the financial system that have gone largely undetected until now. The speed and extent of the Fed’s rate hikes were a key factor leading to the SVB implosion, as the bank invested its deposits in assets highly sensitive to rising rates and with wildly mismatched maturities. This was simply poor asset management, compounded by the fact that their depositor base was mostly comprised of very large corporate clients that would leave large holes if they took their money out. That is just what they did, and so the bank fell victim to a perfect storm of bad management, unfavorable monetary policy and a client stampede. At first glance it appears to be an issue specific to SVB.

The question of why regulators allowed this to happen is getting louder, but it has to be put into context with the intense pressure that banking executives routinely put on lawmakers to loosen bank regulations, blast politicians who dare to recommend the opposite and lobby heavily for more lenient rules. They claim that strong bank regulation is unnecessary and detrimental to the economy. The fact that eliminating it would lower the banks’ compliance costs and improve their quarterly results are never mentioned as a factor.

One thing is clear: The relentless lobbying bought banks much relief when in 2018 Congress passed the Economic Growth, Regulatory Relief, and Consumer Protection Act that, among many other goodies, contained an exemption from automatic supervisory stress tests for banks with assets between $100B and $250B (the range SVB was in). Those who now blame Fed supervisors for being asleep at the wheel with SVB should instead take a look at what kind of issues Congress wanted banks to be supervised for. And it suggests that discussions about whether financial institutions should or should not be allowed to apply ESG (environmental, social and governance) considerations when investing clients’ assets are a gigantic waste of time when efforts can be much more productively deployed in trying to strengthen the financial system against threats to confidence.

Worried about the political fallout, everyone now involved in SVB’s rescue calls it “not a bailout,” noting that the bank’s shareholders and bondholders will not be relieved of their losses.

Fair enough, but the FDIC limit for deposit insurance is $250,000, which reportedly was just a single-digit percentage of SVB’s depositor base. The Fed therefore decided to guarantee all deposits of the failed institution, regardless of size (Roku, the streaming service, had almost half a billion dollars deposited in SVB), saying that the insurance will be covered by the Federal Deposit Insurance Corporation (FDIC) and funded by premiums charged to private banks and not by taxpayer money.

But the Deposit Insurance Fund is backed by the “full faith and credit of the U.S. Government” so public funds are ultimately on the hook, and anyway those premiums are a cost to the banks that will be passed on to everyone using their services, and therefore they will be paid by the public one way or another. The “this is not a bailout” claim is credible only in the narrowest sense. You can call a dog’s tail a leg but it is still a tail.

Of course, it is essential to protect the banking system at any cost and step in aggressively at the first sign that confidence is under attack, so regulators are acting appropriately. But the moral hazard problem will not go away, and it will become a serious one if, like after the 2008 Financial Crisis, there are little if any consequences for reckless behavior and any serious push to strengthen supervision succumbs to industry pressures. For now, however, the questions of culpability and regulation reform will have to wait.

What happens next?

One consequence of the SVB saga is that the Fed will almost certainly refrain from raising rates at the next meeting. This is a huge change from just a week ago, when the market was thinking that a half-percent hike was looking more likely than a quarter-percent hike. As I write this post, the market now is of the mind that the Fed will be done raising rates by May and then it will start cutting them. Lower rates will take a bite of the juicy 5%-plus yields that investors had been enjoying from T-Bills until last week. Those rates plunged by half a percent on the first day after the SVB rescue. Where they go from here is unclear.

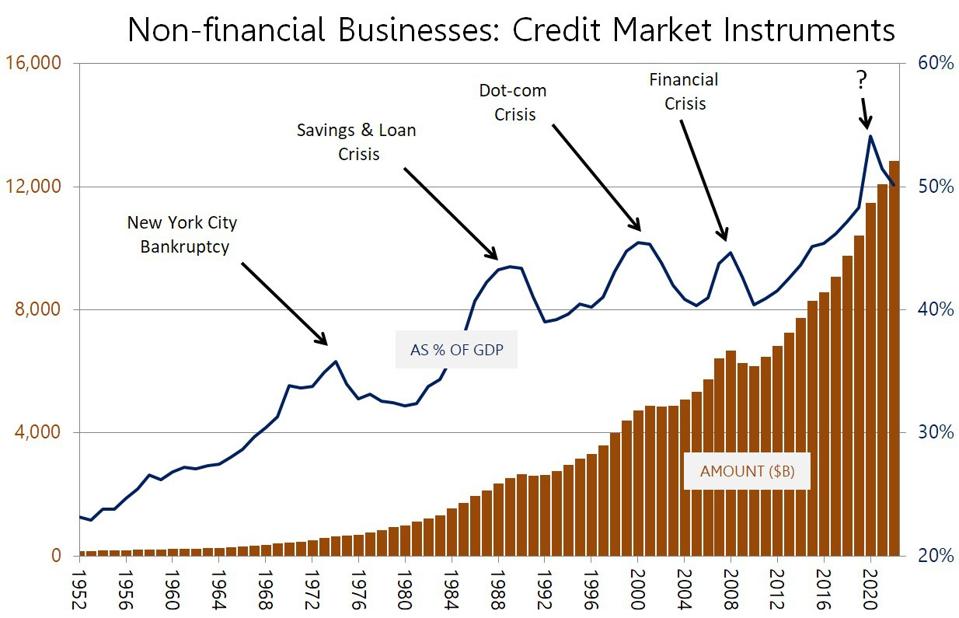

The state of corporate balance sheets will come into sharper focus if fears of contagion spread. A crucial aspect is that corporations outside the financial sector have issued a lot of marketable debt (i.e. corporate bonds) during the years of rock-bottom interest rates. That debt needs to be rolled over periodically, and much higher rates make the new debt considerably more expensive. This could affect corporate credit quality to some degree, further raising the cost of capital. The worst case would be a crisis of confidence that keeps lenders away and precipitates a wave of defaults.

A significant increase in the volume of corporate bonds outstanding tends to trigger a crisis somewhere in the system, as history shows. The amount of corporate bonds is now, by far, the largest in U.S. history and, until recently, also as a % of GDP. The collapse of SVB could be the first sign that a new one is unfolding.

Such crises happened at various points in the past. It seems that when private non-financial debt rises beyond some point, lenders tend to become nervous, liquidity dries out and some headline-grabbing disaster erupts where few are looking. Eventually, though, the connections become clear.

These problems often spread and become systemic because a crisis in the private debt space, if serious enough, triggers a government intervention (i.e. a bailout) that transfers the debt to public hands. Therefore, another consequence of the SVB collapse, if it proves to be the proverbial canary in the coalmine, is that government debt will go up, just when the arguments about trying to bring it under control are heating up.

The lesson from Bear Stearns and Lehman Brothers is that a crisis of confidence tends to unfold in stages. Sure, the implosion of SVB sounds like an isolated, specific issue confined to a small segment of the banking industry rather than the first sign of a broader problem. Alas, it may take a while until we’re really sure.