What Is Transitory Inflation? (1) The Facts

Suddenly – prices are falling everywhere you look. Not just falling, but “plunging,” “plummeting,” “collapsing.”

“Home Prices Fell in November for Fifth Straight Month” – WSJ (Jan 31, 2023) “Apartment rents fell in every major metropolitan area in the U.S. over the past six months.” – WSJ (Feb 27, 2023) “Natural-gas prices plunged…more than 65% since mid-December to their lowest level since 2020’s pandemic lockdown.” – WSJ (Feb 23, 2023) “Used-vehicle values recorded a sharp decline in 2022…The Manheim Used Vehicle Value Index finished 2022 down 14.9%, its worst ever annual result and far worse than the 3% decline forecast at the start of the year.” – WSJ (Jan 10, 2023) “Wholesale egg prices have ‘collapsed’…by more than 50% since December.” – CNBC (Feb 7, 2023)

Yes, the current bout of so-called “inflation” is proving to have been transitory. Definitively, and undeniably.

But what does “transitory” mean exactly? The word has become such a flashpoint in the debate over inflation and what to do about it, that it may now simply serve as a label for what many assume to have been the Federal Reserve’s blundering misdiagnosis of the economy’s trajectory over the past couple years.

“Transitory” has two meanings. One definition is factual, focused on what differentiates “transitory inflation” from other kinds of inflation. Another aspect is the political meaning of the phrase in the messaging war that has engulfed monetary policy in the last several years.

In this column, we will review the questions of fact. In the next column, we will consider the messaging aspects.

“Transitory” Reality

There are six clear truths about “transitory inflation”:

It is caused by disruptions in the supply chain. It is self-correcting. It never leads to “structural” inflation. The Federal Reserve can’t do a darn thing about it. Much of it is not really inflation at all – it is pseudo-inflation. The Fed has been right about the “transitory” diagnosis from the start.

Let’s walk through these points one by one.

1. Transitory Inflation is Caused by Supply Constraints

Inflation is not a unitary phenomenon. A pattern of increasing prices may develop from a number of different causes, and it is important in each case to understand what kind of inflation we are dealing with. A person may run a fever because he has Covid, or leukemia, or malaria, or an E. coli infection – or because he just ran a marathon in warm weather. Getting the diagnosis right is critical, and it requires more than just a thermometer reading. The symptom by itself is not conclusive for deciding what action to take.

Too Many Theories

An economy may run a fever for many differ reasons, as well. Sometimes rising prices are demand-driven (as with housing prices in certain markets like Manhattan or Vancouver). Sometimes inflation is the result of rapid growth in the money supply (although the importance of monetary expansion is controversial). There is the dreaded wage-price spiral where it is said that rising prices stimulate wage demands, which boosts consumer spending, which drives up prices, which spurs further wage demands, which boosts sending even more… etc.

Then there is the theory that inflation causes itself, through the mechanism of public opinion – somehow, inflation today drives expectations of more inflation tomorrow. This causes consumers to engage in “advance buying.” They accelerate the schedule for their purchases from fear of having to pay more in the future, and this demand-drawn-forward adds to inflation today, which further stimulates inflationary expectations, leading to further spending urgency boosting inflation, etc. (This is a quite primitive psychological model, but many economists adhere to it.)

The expectations theory does not explain the current inflationary episode. There is no evidence that either the public or the market professionals have “de-anchored” (as the Federal Reserve puts it).

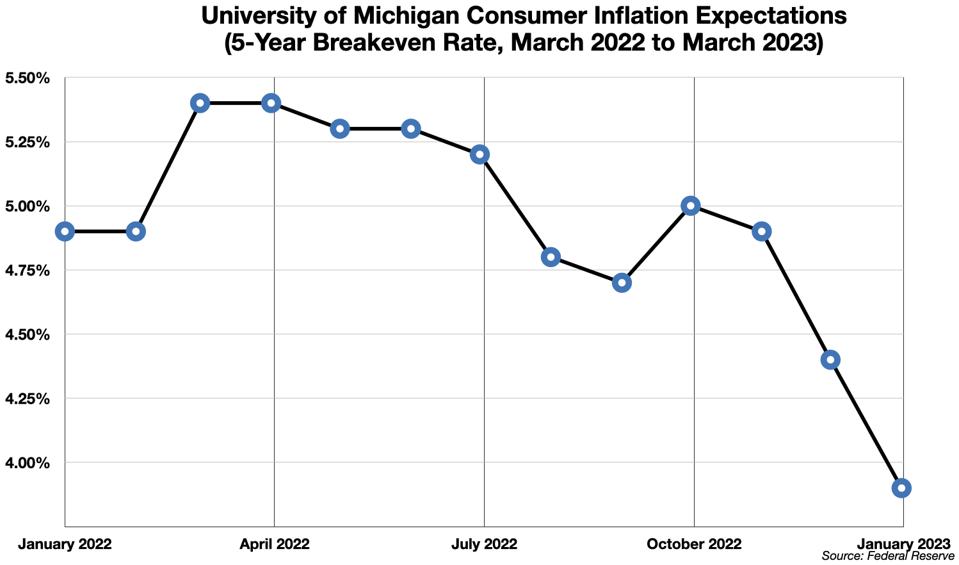

Consumer inflation expectations (which are typically higher than the actual numbers) are moderating over the last year.

Univ of Michigan Consumer Inflation Expectations

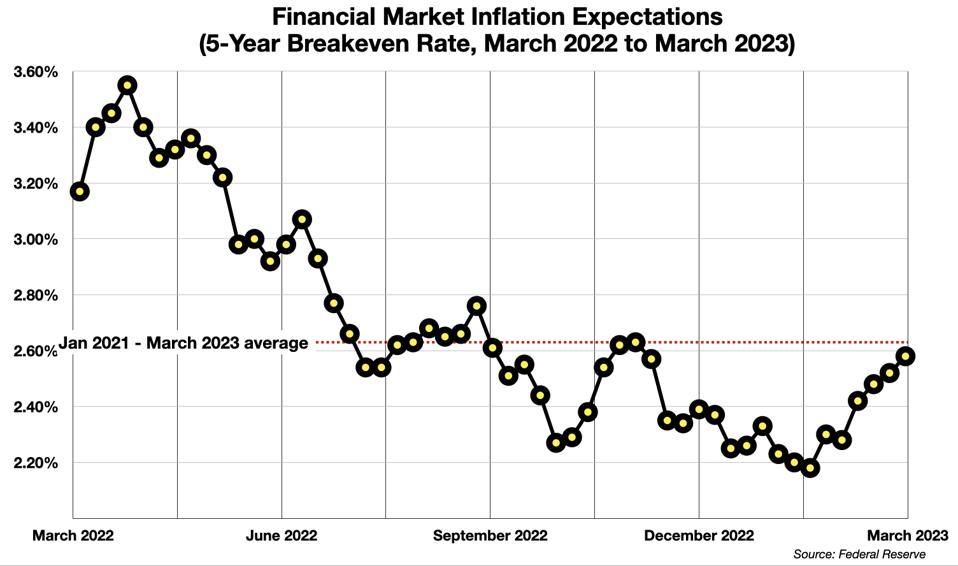

Financial markets project ongoing inflation not far above the Federal Reserve’s target.

Financial Market’s Inflation Expectations

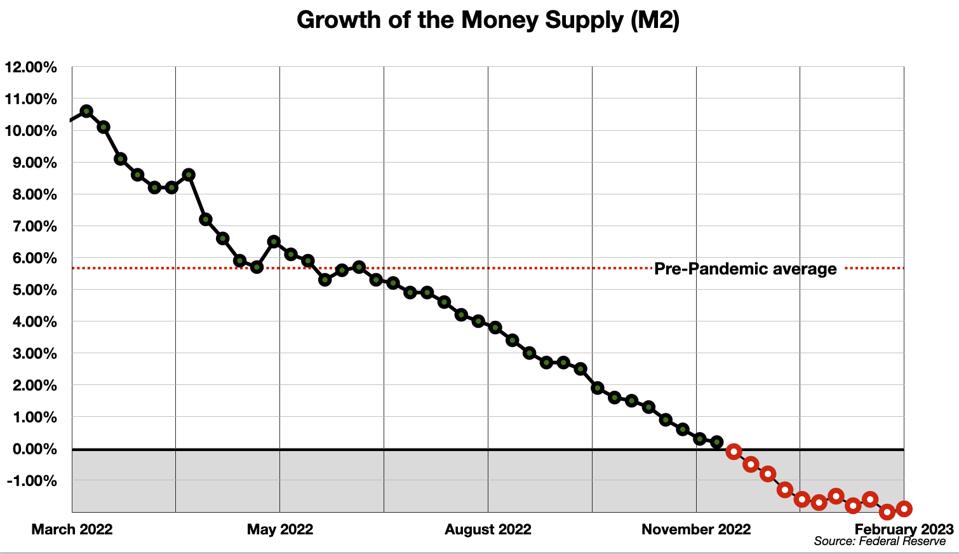

As to the monetarists’ view, the growth of the money supply has decelerated dramatically and has actually gone negative for the first time in history.

M2 Money Supply Over the Last Year

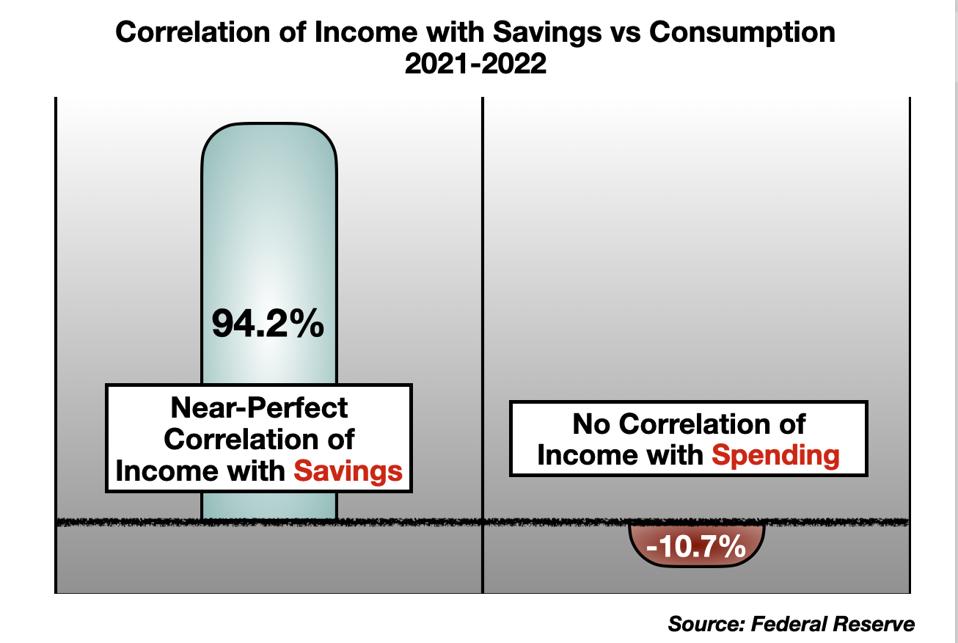

The consumer demand picture is complex, but the gist of it is that the stimulus funds that boosted household income went almost entirely into savings rather than spending.

Correlation of income with savings and spending

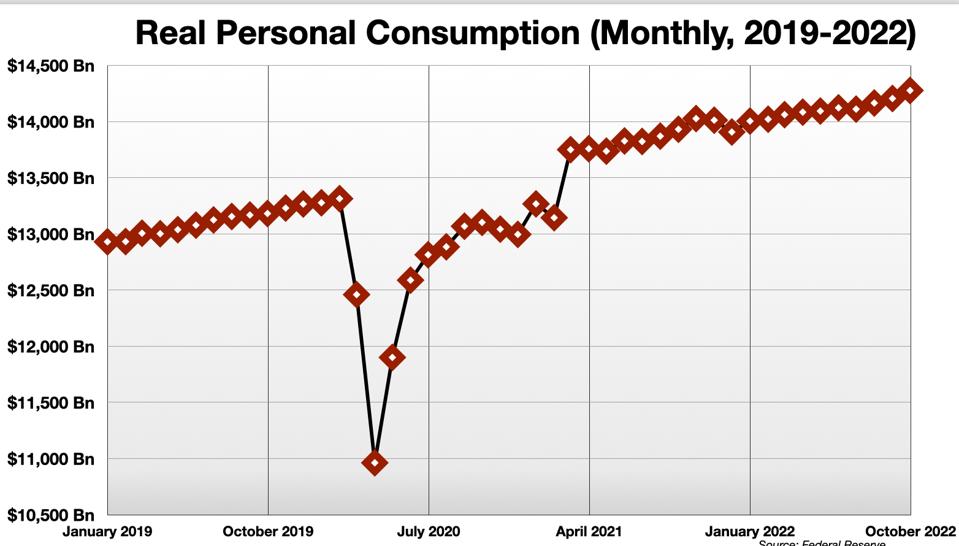

The consumption trend, after it recovered from the down-shock of the pandemic, recovered to its normal trajectory. There was no upwards inflection, and the net effect (including the deficit created by the down-shock) was negative.

Real Personal Consumption

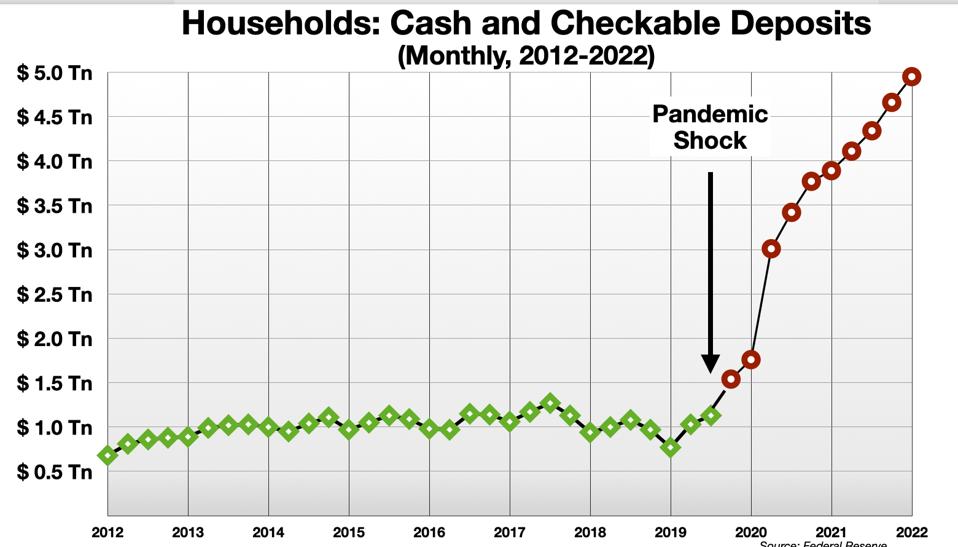

Meanwhile, household savings (cash) tripled.

Household Cash

In other words, whether or not it was “fiscally responsible” to pump $5-6 Trillion off stimulus into the economy, it is apparent that the stimulus did not stimulate. Specifically it did not generate new consumer spending above the trend line. And if it did not boost spending, it could not have caused demand-driven inflation. The price increases were not caused by the stimulus.

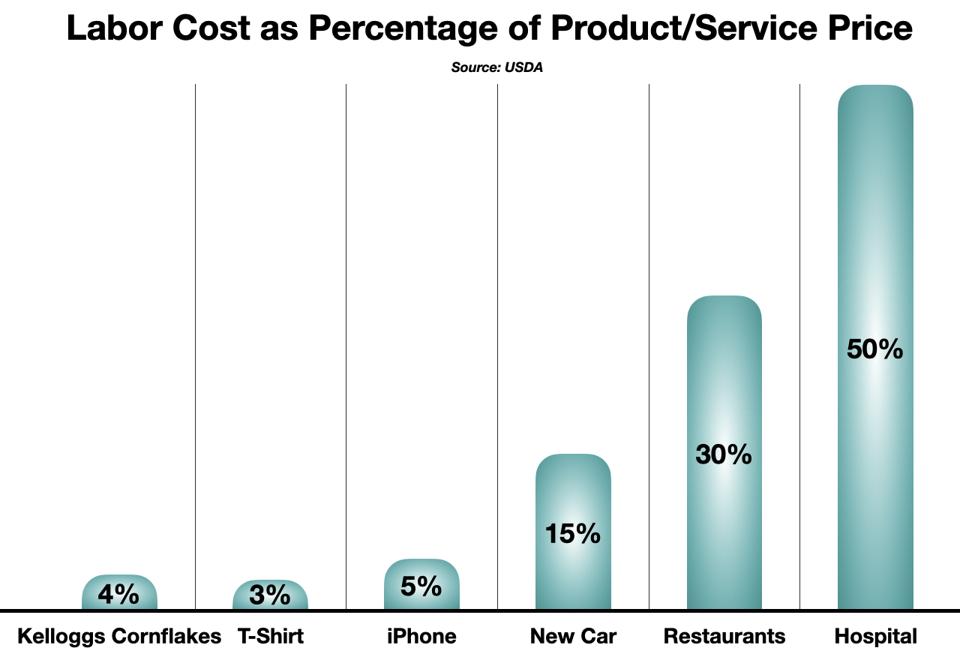

Finally, wages were running at a 3.6% annualized rate in December (and the rate of wage growth has been declining all year). 3.6% may still sound like a lot, but one must examine how much of the cost of labor ends up in the final prices of the goods and services in the CPI.

First of all, there is productivity to consider. Productivity was about 1.7% up in the 4th quarter of 2022. So, the gross “push” from rising wages was less than 2%. And labor costs today are a very small percentage of the cost of most consumer goods. Labor is service sectors is higher, but still not enough to translate into serious inflationary pressure.

Labor Costs as Percentage Of Product:Service Price

3% (labor cost component of a box of cornflakes) of 2% (overall wage push in Q4) is a very small number (~ 0.06%).

Today’s Inflation is Driven by Supply Constraints

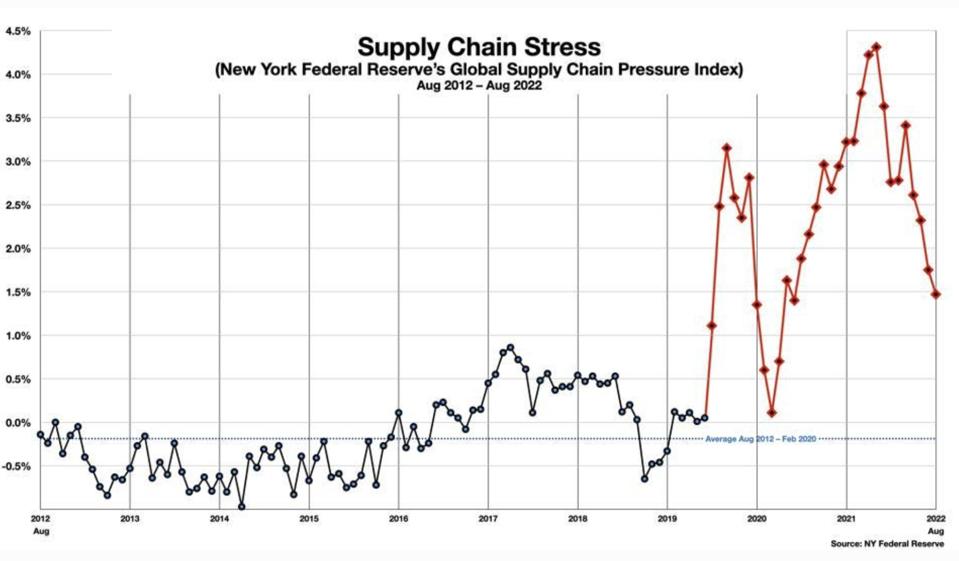

The run-up in prices in the 2021 and the first half of 2022 is not explained by excess stimulus-driven demand, or by the money supply, by wage pressures, or by expectations and other vapors distorting the public psychology. What does explain this episode of inflation are the disruptions of many of the critical supply chains in the economy, from semiconductors and gasoline to eggs and used cars. In all of these cases, the price problems are clearly the result of anomalous (and severe) supply shocks. The Federal Reserve has a new measure of supply chain stress, which makes this clear.

Supply Chain Stress

2. Transitory Inflation is Self-Correcting

Markets seek equilibrium between supply and demand. Imbalances do arise, of course, and prices send signals to producers and consumers who adjust their behavior in ways that tend to restore the balance. In the case of supply-driven inflation, the response of the market is realized as producers move to eliminate the bottlenecks and restore normal supply conditions.

As the opening quotes from the recent press accounts make clear, many prices are now coming down, violently in some cases. Words like “collapsing” and “plunging” and “worst ever declines” are proliferating to describe price trends in sector after sector. This is the other sign that the price bubbles in energy, used cars, eggs and the like were caused by supply constraints: the shortages are often followed by gluts, as the supply side of the market overcompensates.

In fact, it is happening today in almost all major commodities, as described in another recent column.

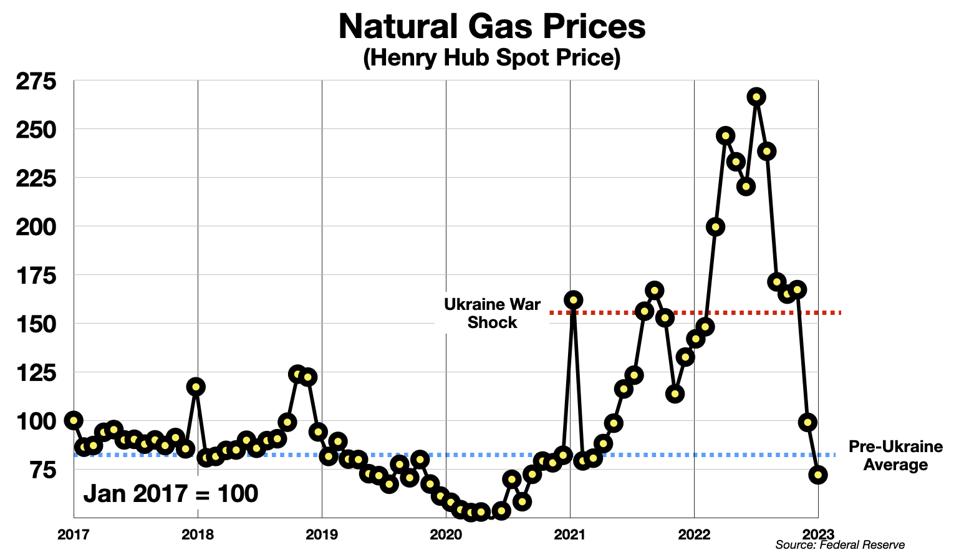

Natural gas is a clear example. The supply shock in this case was the Russian invasion of Ukraine. Every markets were thrown into dislocation by the various events surrounding the question of gas supply to Europe. Prices skyrocketed. But producers responded, building new LNG terminals in record time, expanding exports from the U.S. and rerouting other links in the supply chain. The result was deflation.Natural gas prices have fallen back to their pre-pandemic level.

Natural Gas Prices

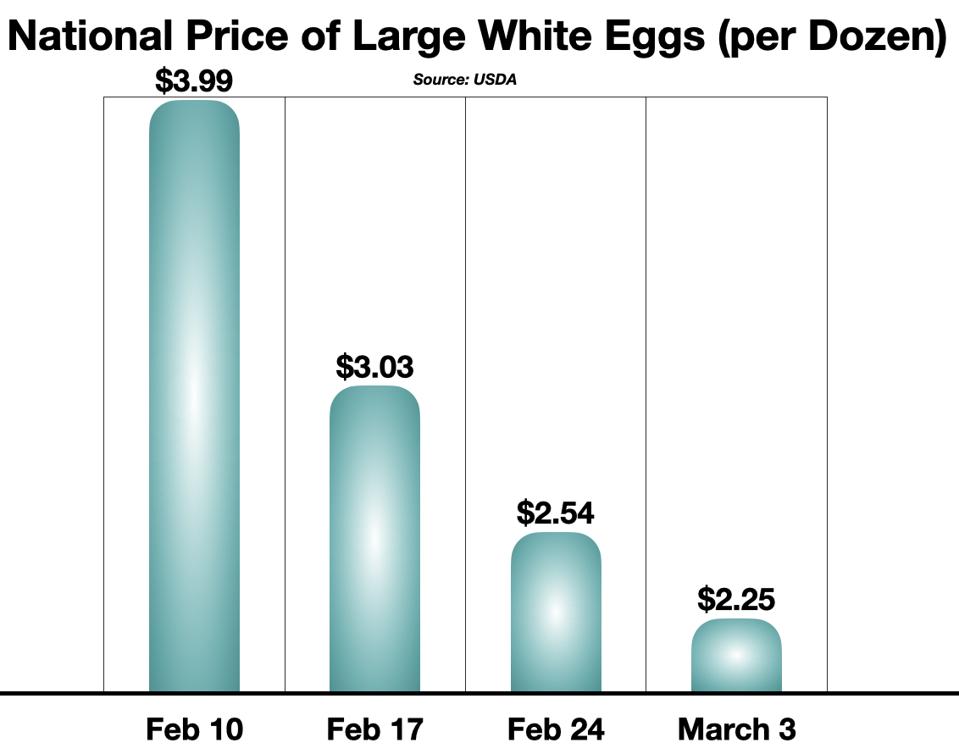

Another star of recent inflation panic-narrative shows the same pattern – sudden deflation with a vengeance.

Egg Prices in Last 30 days

Housing, energy, and many commodities all show deflationary trends today. In the coming months, barring another supply shock, this will become even clearer in many sectors of the economy.

The failure of these supply bottlenecks to ignite structural inflation should not be surprising. The consumption habits for products like gasoline and food are stable and slow-changing. The production systems that deliver them are finely tuned, and designed to adapt fairly quickly to disruptions — even disruptions as severe as the Covid pandemic and the Ukraine War.

3. Transitory Inflation Does Not Lead to “Structural” Inflation

A corollary of the self-healing dynamic of transitory inflation is that the impact of such price increases is…well, transitory. As bottlenecks are broken, prices first decelerate (“disinflation”), and then may actually fall (“deflation”). Price levels often return to some more or less “normal level” as the supply constraints are alleviated. In any case, temporary supply crises do not lead to “structural” inflation.

What then is structural inflation, the bogey feared by so many?

It occurs (or is said to occur) when something “fundamental” changes the patterns of supply and/or demand in the real economy, and puts pressure on prices that is sustained and irreversible. For example, the emergence of China from the Covid “recession” later this year may create substantial incremental demand that could push up prices for certain commodities.

However, most structural trends and shifts are deflationary. Technology, demographics, globalization, all tend to drive prices downward over the longer term.

Price increases caused by temporary shortages are (as noted) self-correcting. The market’s equilibrium-seeking process is very powerful. There is no theoretical mechanism by which “transitory” can somehow mutate into “structural.”

4. The Fed Is Helpless To Deal With Transitory Inflation

A central bank has a limited toolkit with which the influence the economy. It can raise or lower certain short-term interest rates. It can buy or sell bonds or other securities, which either injects or withdraws liquidity. It can disrupt and depress the psychology of the financial markets. It can talk tough. But it cannot actually force banks to lend, or force consumers to borrow and spend. And it can do nothing at all to address shortages of semiconductors or eggs or anything else in the basket that makes up the Consumer Price Index. (Please note that mortgage payments, the one consumer expenditure that is said to be most directly impacted by the Fed’s rate increases, are not a component of the CPI.)

This essential impotence of the Central Bank to address the causes of this kind of inflation – the “transitory” kind – is well understood by Fed officials. As Powell has admitted, “There’s really not anything that we can do about oil prices.” Or used cars, or eggs. In Senate testimony last year, Powell told it like he saw it:

Jerome Powell: We don’t have much ability to affect the supply side. And if you look at where the really big contributors are to the overshoot from inflation, it’s in the goods sector still, largely and that’s cars that’s new, used, and rental cars, it’s appliances. Sen. Mike Rounds (R-S.D.): What about food? Hamburger at over $5 a pound? Powell: I’d say that there are supply side issues there too, as you and I have discussed, but those are really outside the range of our of our tools. Sen. Rounds: Is it fair to say petroleum products as well, the price of gas over $5 a gallon. Those are items that are supply side. They’re not the demand side. The supply side of this is a significant part of the entire inflationary demand. Powell: That is right.

In the face of this, the Fed has pursued performative policies designed to safeguard its institutional credibility, which is perhaps its chief asset. In the pandemic, the Fed’s responses helped maintain confidence in the functioning of the financial system, and spurred the public’s rapid psychological recovery from an unprecedented series of shocks. The Fed’s role as a backstop in market panics is critical. But it doesn’t mean the bank can do anything about the price of eggs.

5. Pseudo-Inflation

Some of what we call inflation is not really inflation at all. I term it pseudo-inflation. These are cases where a rise in prices is so temporary, and so unrelated to any of the traditional causal factors, that it should really be removed from the overall calculation.

For example, we have become accustomed to “surge pricing” for services like Uber. Or similar pricing games played by the airlines or by Amtrak – they it call “revenue management.” [I travel regularly from Washington DC to New York by Amtrak, and depending on how and when I purchase my ticket, the cost can vary by a factor of 4 to 6 times (for the same train). No one would suggest injecting this volatile signal into the CPI.]

But there are cases where I would argue that components of the CPI do exhibit . The best example of pseudo-inflation is the recent surge in the price of eggs.

MORE FROM FORBESThe Federal Reserve Has An Egg Problem – And A ‘Chicken-And-Egg’ ProblemBy George CalhounMORE FROM FORBESIs Inflation Created By Corporate Greed? Evidence From The Current Egg-Flation EpisodeBy George CalhounMORE FROM FORBESThe ‘Egg Crisis’ – Another Pseudo-Inflation PhenomenonBy George Calhoun

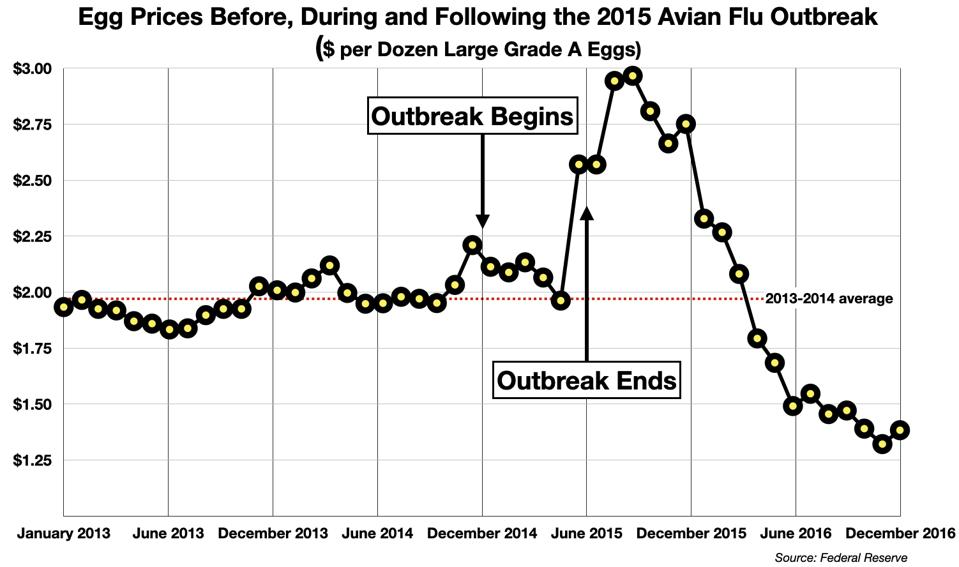

Egg prices have been extraordinarily stable for decades, in nominal terms. The posted price of a dozen eggs just prior to the pandemic shock was the almost the same as it was in 1984. (Of course in “real” terms, adjusted for inflation, the price of eggs has plummeted.)

This pattern has been broken twice. In 2015, a bird flu epidemic that killed 50 million hens caused egg prices to spike by 50%. But the market soon recovered. Supply was restored (and then some – a glut soon followed, with a price collapse). Here is what the 2015 episode looked like.

Avian Flu Outbreak in 2015

This is pseudo-inflation. It was not caused by changes in demand, changes in the money supply, consumer inflation expectations, or a wage-price spiral. It was not caused by changes in cost of the inputs to the egg production process (e.g., feed, power, transport, labor). It was caused by a virus that decimated the egg-laying flocks. It did not result in a permanent increase in egg prices.

The market worked. A smarter version the CPI would recognize this, and eliminate it from the calculation. In fact, there are several adjusted versions of the CPI designed by Federal Reserve economists to eliminate the effects of outliers and anomalies. Unfortunately, the media does not report on these “smart” indices. Instead, it is the dumb version – the unadjusted CPI – that dominates the news channels every month.

Pseudo-inflation has affected many other important components of the CPI, including most energy prices (natural gas, gasoline especially, jolted by the Ukraine war), many food components, used cars. Exogenous shocks have created supply chain dislocations, shortages, and obviously temporary price spikes. These outliers have distorted the CPI, causing inflation to seem hotter than it really is.

6. Did the Fed blunder?

I believe the Fed’s economists, and the Chairman, are well aware that this post-pandemic inflationary episode is indeed “transitory.” I think they probably also understand most of the facts about transitory inflation described above.

The Fed has a weak hand to play in today’s inflation game. It can’t do anything to directly affect the supply bottlenecks, so officials have concentrated on bolstering their institutional credibility, talking tough, and fighting against the possibility that inflationary expectations could ignite. (Whether those expectations have any real role in driving real inflation is doubtful, but perhaps it doesn’t do any harm to press the point, as Powell and his colleagues have been doing.)

The recent easing of rate increases (from four straight 75 basis point hikes last summer and fall, to just 25 basis points most recently) is evidence that collectively the Fed understands much of what is going on here. As supply shortages are alleviated, the transitory character of inflation will become clear. Lately, though, the messaging has changed, which creates some confusion. We will examine this aspect of “transitory” in the next column.